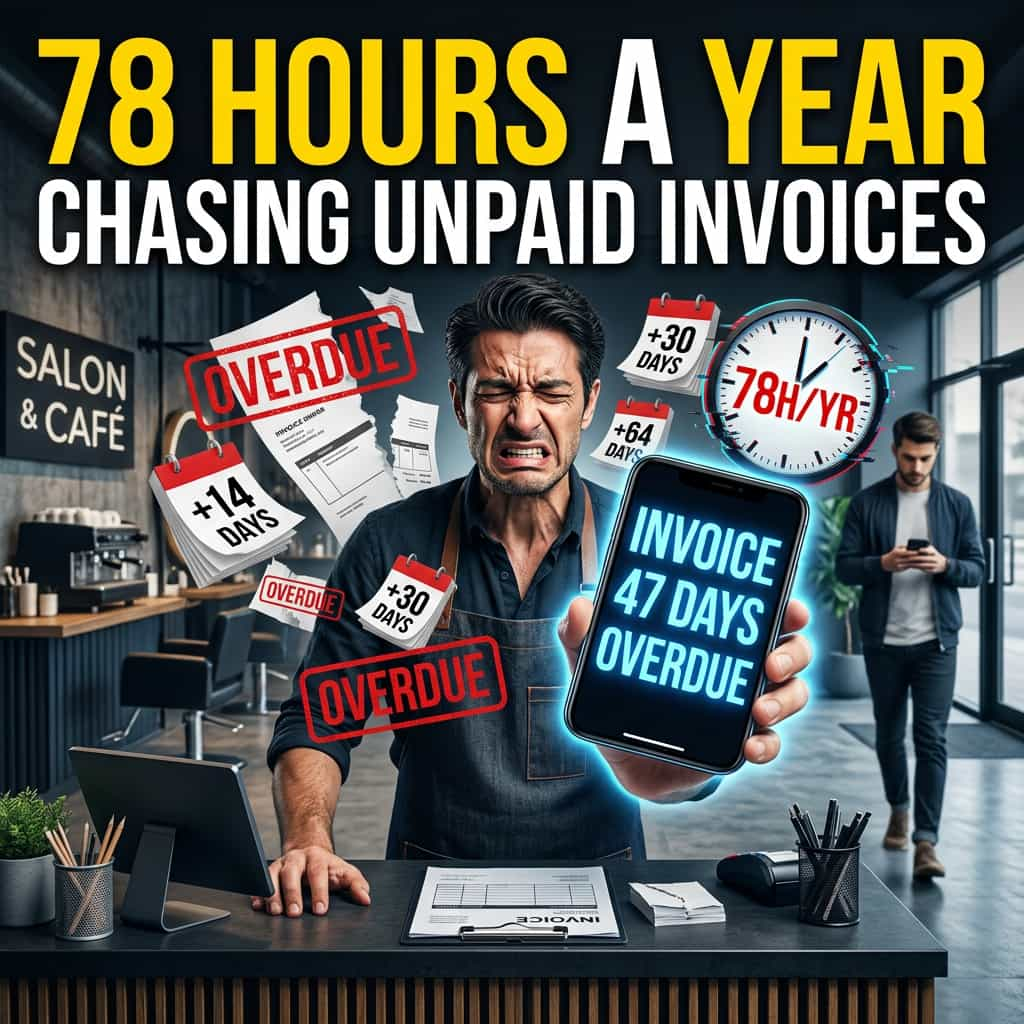

It's Tuesday afternoon. You've sent the same polite reminder for the third time. The invoice was due 47 days ago. The customer is one of your bigger ones, and you don't want to seem rude. So you wait. Again.

Across Australia, this scene plays out in salons, cafés, trade depots, dental practices, and small consulting offices every week of every quarter. New research from GoCardless, conducted by YouGov in late 2025 and released in full on 11 March 2026, surveyed 500 Australian SMB owners and found that the 63% who chase late payments lose an average of 1.5 hours a week doing so — about 78 hours a year, or close to two full working weeks. (These numbers come from GoCardless. The survey was conducted by YouGov independently, but GoCardless commissioned it and sells a payment tool that benefits if more businesses move away from manual chasing. Read the figures with that lens. The pattern, however, is corroborated by Australian government data — see the next section.)

This is not a vendor pitch dressed as a stat. The Australian Government's Payment Times Reporting Regulator confirmed the same trend in its January 2026 update.

This post explains, in plain English, what the GoCardless and government numbers actually say, why the late-payment crunch is getting worse for small businesses specifically, and four things you can do this week to claw back time and money you're losing right now.

The government numbers say it's getting worse

Twice a year, large Australian businesses (those with turnover above $100 million) are required by law to report how quickly they pay their small-business suppliers. The Payment Times Reporting Regulator publishes the data. The January 2026 update covers the reporting period 1 January to 30 June 2025.

The headline: across all industries, only 66.5% of invoices to small-business suppliers were paid on time. The slowest 5% of invoices (the 95th percentile measure) took 64 days on average — up from 58 days in the previous reporting period. Healthcare and social assistance was the worst offender, with only 60.3% of invoices paid on time. Agriculture, forestry and fishing was the strongest, at 73.4%.

The trend is going in the wrong direction. The slowest payers are taking longer. The number of small-business suppliers waiting more than two months for payment has grown.

That is the government-confirmed half of the story.

What 500 SMB owners told YouGov

The GoCardless / YouGov survey adds the lived-experience half. Some highlights, all weighted to ABS business population estimates:

- 69% of Australian SMBs received late payments in the past year. Up from 63% in 2024.

- 48% are waiting longer for payments than they were 12 months ago.

- 41% wait more than 14 days past the due date on average. 17% wait more than a month.

- 23% of Australian businesses said they would write off 6% or more of annual turnover to avoid the awkward conversation. Among Gen Z and Millennial owners, that figure is 38%.

- 34% turned to credit cards or loans in the past year specifically because late payments hurt cash flow.

Two patterns matter here for the petshop owner reading this.

First, late payments are no longer a "rough year" exception. They have become a baseline cost of doing business. 68% of Australian SMBs now agree late payments are "an inevitable cost of doing business." That mindset is the trap.

Second, the time cost is concentrated. The 78-hours-a-year figure applies to the 63% of businesses that actually chase. If you are in that group, two whole weeks of your year goes to chasing money you are already owed. That is two weeks you could have spent on the work that actually pays.

Why this hits small businesses harder than big ones

A bigger business with proper finance staff and a credit-control function absorbs late payments. A salon owner with five staff cannot.

When an invoice is 64 days overdue, the salon owner is paying staff, rent, and supplier accounts on time, from their own working capital. The customer's delay quietly becomes the salon owner's debt — and 34% of AU SMBs ended up on credit cards or loans because of exactly this. The owner spends Tuesday afternoon writing reminders instead of doing the work that pays. The conversation gets harder the longer it is avoided. 38% of AU SMB leaders who avoided the conversation reported increased workplace stress; 36% reported increased personal stress.

This is the unglamorous side of the cash-flow crisis everyone keeps writing about. It is not headline-grabbing. It is just real, measurable, and — crucially — fixable.

What stops it

Three things are working right now for Australian small businesses. None of them are silver bullets. All of them are within reach.

1. Pull-based payment methods.

Direct Debit, PayTo, and similar tools take the act of paying out of the customer's hands. Once the customer signs the authorisation, the funds are pulled on the day they are due. No reminder. No conversation. No 64-day blowout. This is the most reliable fix, and it is why GoCardless and similar vendors exist. Read the GoCardless framing for what it is — they sell this — but the underlying mechanism (Direct Debit / PayTo) is bank-rail technology, not a vendor-locked feature.

2. Automated invoice reminders.

Every major Australian accounting platform now has this. MYOB launched its Smart Invoice Reminders feature on 1 March 2026 — it suggests when to chase, what tone to use, and sends customisable follow-ups based on each customer's late-payer pattern. Xero has had similar automation for some time. We covered MYOB's broader AI rollout in last week's post on the manual-reconciliation problem. If you are already on MYOB or Xero, the reminders are likely sitting inside your subscription, switched off.

3. eInvoicing through the Peppol network.

Australian government and many large enterprises now process invoices delivered through the Peppol e-invoicing network. Peppol invoices land directly inside the recipient's accounts payable system, eliminating the "we never got the invoice" excuse. The ATO has been quietly pushing this for years. If you supply to government or large corporates, this alone reduces payment friction.

None of these stop the customer who simply will not pay. But they remove the excuses, the friction, and the silent admin tax of chasing.

What you can do this week

1. Switch on automated reminders inside your existing accounting software.

If you are on MYOB, Xero, or QuickBooks, this is already in your subscription. It takes about 20 minutes to set up a three-stage reminder cadence (day after due, week after, two weeks after). Most owners discover it was never enabled.

2. Pick one customer who pays late every month and offer them Direct Debit.

Frame it as "easier for both of us." Most repeat-late customers will say yes. One Direct Debit setup ends a recurring 30-day chase forever.

3. Add late-payment terms to your invoice template.

A simple line — "Payment is due in 14 days. Overdue invoices may attract a 1.5% monthly late fee." — changes the conversation. You don't have to actually charge the fee. Putting it in writing changes how seriously the invoice is treated.

4. Have one money conversation you have been avoiding this week.

The GoCardless data shows avoidance is the most expensive habit Australian small business owners have. Pick one customer. Send a calm, friendly, direct message about the overdue invoice. The conversation is almost never as bad as the avoidance.

If you are not sure where to begin with any of this, our earlier post for owners who don't know where to start is the right next read.

Two honest caveats

First, the GoCardless 78-hours-a-year stat is from a vendor-commissioned survey. The methodology — YouGov-conducted, 500 AU SMB decision-makers, weighted by ABS data — is sound. But the 78 hours specifically applies to the 63% of businesses that actively chase. If your bookkeeper handles all of it for you, the time cost shifts to them and the bill arrives as their invoice instead.

Second, the Payment Times Reporting Regulator data covers payments from large entities to small-business suppliers. If your customers are mostly other small businesses or consumers, this government data does not directly describe your situation. The crisis still applies, but the specific 64-day figure is for the supply-chain-to-large-business slice.

The point is the same either way. Late payments are real. The cost is measurable. And the tools to stop bleeding time exist already inside the subscription you are paying for.

You just have to switch them on.